FALMOUTH, Maine — If you have a mortgage and/or student loan debt, you may be able to get a temporary break under certain provisions of the Federal CARES Act. The deferment plans for student loans appear to be pretty straightforward. But when it comes to mortgage deferments, or forbearance as it is also called, there's confusion and questions about whether the plans being offered are providing the relief intended.

As of March 13th, federal student loan payments are suspended until September 30, 2020. Interest will not accrue during that time. And if you decide to make a payment during that time, 100-percent of it will go toward the principal of the loan. For more information, visit the Department of Education's Federal Student Aid website.

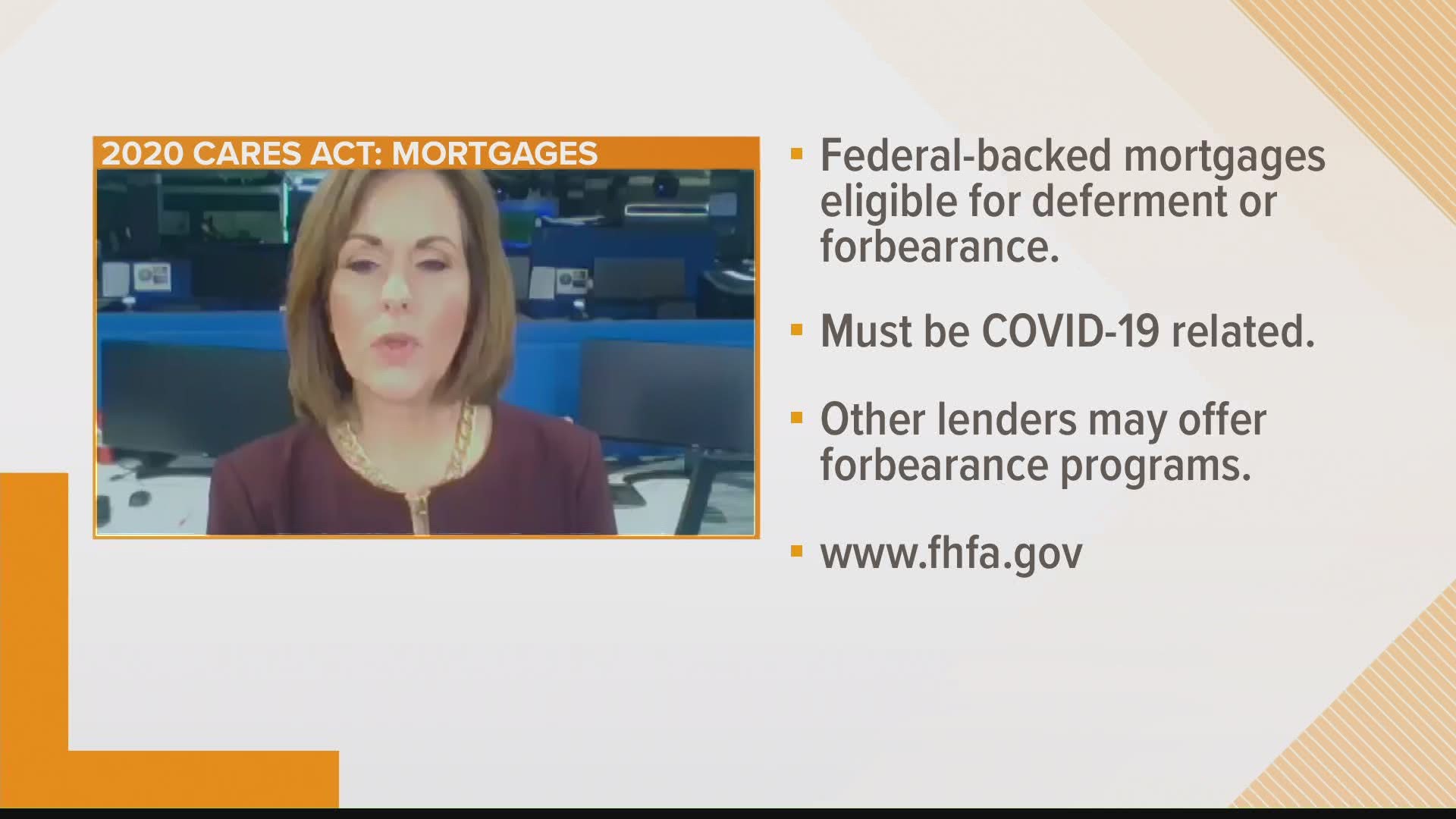

The CARES Act also requires mortgage servicers to provide forbearance, or a temporary postponement of payments, to anyone with a federally-backed mortgage. Some servicers of other mortgages may also offer forbearance plans at their discretion. But Certified Financial Planner Sarah Halpin of Back Cove Financial in Falmouth cautions, "Make sure you understand the new terms clearly." Seemingly wise council since, as recently reported in USA Today, there is some confusion about how long borrowers have to pay the money back, and under what circumstances. Many homeowners report that they have been told they will have to pay a lump sum at the end of the forbearance period to make up for the missed payments, a situation that is causing more stress and anxiety than it is relieving.

If you are considering asking for a deferment or forbearance on your mortgage, Halpin suggests you first visit the Consumer Financial Protection Bureau's website to do your homework.

Below is Halpin's full action plan for those facing financial crisis.

Action Plan: Making Sound Financial Decisions When Faced with Financial Uncertainty Presented by Sarah J. Halpin, CFP®

Life happens. Events you did not foresee will occur. These are stressful times, so you want to make sure that you are making informed and sound financial decisions appropriate for the “here and now” that also stand the “test of time” when you look back. Below are some steps and tips to help you create an action plan for this moment. Make sure you talk with your partner, if applicable, and commit to working as a team to create a family action plan to secure a positive financial future.

Step One: Take Control

This is an important time to get a handle on your major financial resources and debts in order to make a financial plan that works for you and your family. In order to do this, you should prepare a net worth statement. This is a list of everything you own (assets) and everything you owe (liabilities). It helps to group assets into categories: cash, invested assets, and use assets (home, cars, etc). Then list your liabilities in order of their maturity date (when the final payment is due). Now subtract your liabilities from your assets to determine your net worth.

Tip: Update your net worth statement at least annually. Your net worth statement provides a snapshot of how you are progressing towards your financial goals. Hopefully, your assets will increase over time and your liabilities will decrease, ensuring a greater net worth number. This is a sign of financial strength!

Step Two: Analyze Spending

Checking your monthly budget, or creating one, can help you and your family find opportunities to lower expenses and save more by analyzing your cash flow. Cash flow refers to the income coming to your household and the money flowing out each month. To get started, track all your sources of income after taxes and total these. Then time for the less glamourous part, looking back at your spending! Look back over the past three months and categorize your expenditures by fixed costs and discretionary costs. The fixed costs are the essential monthly expenses— usually shelter, food, utilities, insurance, and transportation. This is essential because it shows you the minimum amount of money you need to live on. Add in your discretionary spending and contributions to savings, then calculate. Looking at the past three months to determine your monthly cash flow will help you catch any expenses that are not monthly but should be accounted for, like quarterly bills. The difference between your income and all the month’s expenditures shows your financial flexibility for the month and will confirm if you are “living within your means”. Now you can create a future spending plan with savings and security as your top priority.

Tips:

- When looking to reduce expenses, review your autopay spending on your bank and credit card statements.

- Find the method to track monthly spending that makes you want to do it! Use worksheet tools, create your own spreadsheet, or use personal finance apps such as Mint and You Need a Budget (YNAB). Don’t keep your budget hidden! Keep it in sight along with calendars and to-do lists.

Step Three: Conserve Cash

Be prepared for uncertain times. An “emergency fund” is a savings account you keep in case any unexpected life events come up that threaten your financial stability. I recommend maintaining – or working towards having – an emergency fund equal to six months of fixed expenses. In a recession, you may want to hold an amount that could cover eight to nine months of expenses. If you have gotten this far, you now know the minimum amount of money you need to live on. For example, if your fixed expenses are $3,000 per month, you would want to have an emergency fund of $18,000 -$27,000. Your cash emergency fund should be held in an easily accessible bank, credit union, or online money market account so that you can access it quickly if you need to. Having a chunk of money set aside at the bank increases feelings of control during a financial crisis and can decrease stress during life’s tough moments.

Tip: Consider adding an additional amount to your emergency fund for potential out of pocket health expenses, especially if you have a high-deductible health insurance policy.

Step 4: Manage Your Debt

A financial crisis is less stressful when you and your family are not carrying a lot of non-mortgage debt. However, if cash flow is tight in this moment, now may be the time to pay the minimum payments on your debt in order to maintain a higher cash reserve. The Coronavirus Aid, Relief, and Economic Security Act (the CARES Act) was signed into law on March 27th, 2020. Take the time to review and seek out resources if you have questions. Components of the Act’s relief provisions includes:

Borrowers of federal student loans will not be required to make student loan payments prior to September 30, 2020, and interest on the loans will not accrue during this time period. For more information, visit the Department of Education’s Federal Student Aid website, which provides guidance for students, borrowers, and parents during the coronavirus outbreak.

The CARES Act has provisions affording individuals the ability to defer mortgage payments under certain circumstances. This relief is limited to loans backed by the federal government. More information and resources on mortgage payment relief is available from the Federal Housing Finance Authority

- The 10% early-distribution penalty tax that would normally apply to IRA distributions made prior to age 59½ (unless an exception applies) is waived for retirement plan distributions of up to $100,000 relating to the coronavirus; special re-contribution rules and income inclusion rules for tax purposes apply as well.

- Limits on loans from employer-sponsored retirement plans are expanded, with repayment delays provided. Contact your employer’s Human Resources department or the retirement plan administrator for more information on plan loans.

Tips:

- Weigh all of your options before taking distributions from retirement accounts. Withdrawals could have a long term negative impact on your retirement plan. Reducing your expenses, using your cash reserve or looking into home equity line may be better short term alternatives.

- Use a website such as www.annualcreditreport.com to request your credit report and maintain your score. Make credit payments on time and in-full and keeping your utilization rate (balance-to-limit ratio) as low as possible are the best ways to maintain your credit score. At a maximum, you should try to keep your credit card balances below 30 percent in total and for each individual card.

- Talk to your lenders. Keep in mind, lenders don’t want you to fall behind on your payments any more than you do. If you’re facing trouble making monthly payments, contact your lender or creditor. They may have options for helping you cope with COVID-19-related financial hardships. For example, lenders can place your accounts in forbearance or deferment for a period of time.

- Use credit as a financial tool. While debt is a problem, credit can be a financial tool that can help improve your overall financial health in the long run. As always, avoid making rash decisions when it comes to credit and your financial health.

Information is provided for informational purposes only and should not be relied upon for tax or legal purposes.

Securities and advisory services offered through Commonwealth Financial Network®,

Member FINRA/SIPC, a Registered Investment Adviser.

--

At NEWS CENTER Maine, we’re focusing our news coverage on the facts and not the fear around the illness. To see our full coverage, visit our coronavirus section, here: www.newscentermaine.com/coronavirus.